2026 Retirement Account Contribution Limits: Essential Guide for Those 50+

- Kyle Rolek, Retirement Planning Specialist

- Nov 16, 2025

- 4 min read

Updated: Nov 25, 2025

The IRS has announced higher contribution limits for 2026, giving those ages 50 and above more opportunities to boost their retirement savings.

If you're approaching retirement, understanding these changes—especially the enhanced catch-up provisions—can help you maximize your tax-advantaged savings in the final stretch.

401(k), 403(b), and 457 Plans: Room to Save More

Standard Contributions

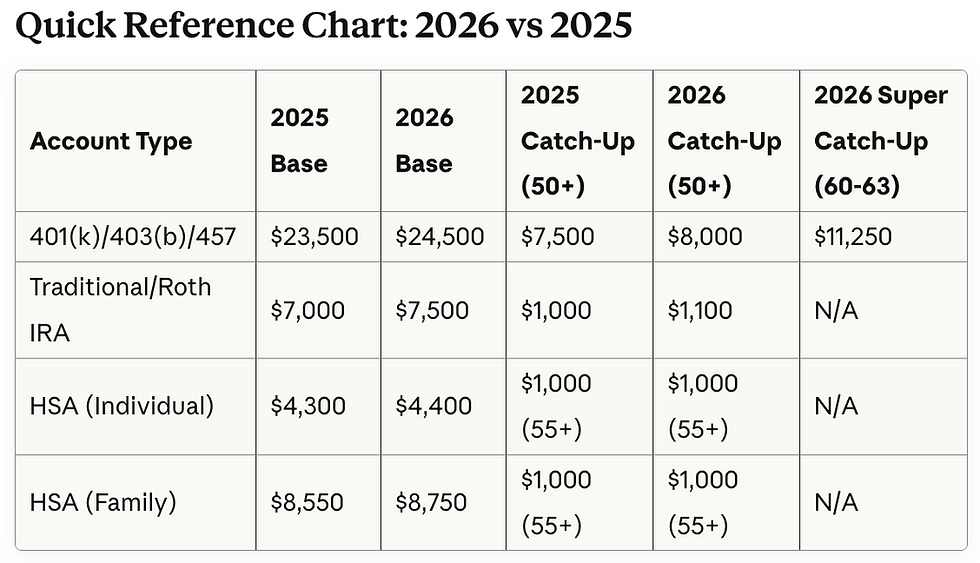

The base contribution limit for workplace retirement plans is increasing across the board:

2026: $24,500

2025: $23,500

Increase: $1,000

This limit applies to 401(k) plans, 403(b) plans, most 457 plans, and the federal Thrift Savings Plan.

Age 50+ Catch-Up Contributions

If you're age 50+ by December 31, 2026, you can make additional catch-up contributions:

2026: $8,000

2025: $7,500

Increase: $500

Combined with the base limit, workers age 50+ can contribute up to $32,500 in 2026 ($24,500 + $8,000).

Super Catch-Up for Ages 60-63

Specifically for those in their early sixties, the SECURE 2.0 Act created an enhanced catch-up provision specifically for workers aged 60, 61, 62, or 63:

2026 Super Catch-Up: $11,250

2025 Super Catch-Up: $11,250

No change from 2025

If you turn 60, 61, 62, or 63 during 2026, you can contribute up to $35,750 total to your 401(k), 403(b), or similar plan ($24,500 base + $11,250 super catch-up).

This enhanced catch-up amount replaces the standard $8,000 catch-up for this age group.

Once you turn 64, you revert to the standard age 50+ catch-up limit.

The four-year window between 60 and 63 provides a critical opportunity to accelerate your retirement savings during your peak earning years.

Starting in 2026, 401k and 403b catch-up contributions must be made as Roth contributions for those with wages in excess of $145,000 for 2026.

Traditional and Roth IRAs: New Limits After Years of Stagnation

Standard Contributions

After remaining flat for several years, IRA limits are finally increasing:

2026: $7,500

2025: $7,000

Increase: $500

This limit is per person. Married couples can both contribute these amounts assuming they meet income eligibility requirements.

Age 50+ Catch-Up Contributions

The catch-up contribution for IRAs is also getting its first inflation adjustment under the SECURE 2.0 Act:

2026: $1,100

2025: $1,000

Increase: $100

Individuals age 50+ can contribute a total of $8,600 to their IRAs in 2026 ($7,500 + $1,100 catch-up) assuming they meet income eligibility requirements.

Important Notes on IRA Contributions:

Unlike 401(k) plans, IRAs do not have a super catch-up provision for ages 60-63. All savers age 50 and above receive the same $1,100 catch-up allowance.

See Roth IRA income limits here: Roth IRA Income Limits

See Traditional IRA deduction income limits here: Traditional IRA Income Limits

Health Savings Accounts (HSAs): Triple Tax Advantages

HSAs offer unique benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

For those 55 and above, these accounts become even more valuable.

2026 HSA Contribution Limits

Individual Coverage:

2026: $4,400

2025: $4,300

Increase: $100

Family Coverage:

2026: $8,750

2025: $8,550

Increase: $200

Age 55+ Catch-Up Contributions

If you're 55+, you can contribute an additional $1,000 (no change from 2025)

This means individuals 55+ can contribute up to $5,400 (individual) or $9,750 (family) in 2026.

HSA Eligibility Requirements

To contribute to an HSA, you must be enrolled in a high-deductible health plan (HDHP).

For 2026, minimum annual deductibles are:

Individual coverage: $1,700

Family coverage: $3,400

Maximum Contribution Totals for 2026

Age 50-59:

401(k)/403(b): $32,500

IRA: $8,600

HSA (individual): $5,400 (55+ only...50-54 is $4,400)

HSA (family): $9,750 (55+ only...50-54 is $8,750)

Age 60-63:

401(k)/403(b): $35,750 (with super catch-up)

IRA: $8,600

HSA (individual): $5,400 (55+ only...50-54 is $4,400)

HSA (family): $9,750 (55+ only...50-54 is $8,750)

Age 64+:

401(k)/403(b): $32,500 (reverts to standard catch-up)

IRA: $8,600

HSA (individual): $5,400 (55+ only...50-54 is $4,400)

HSA (family): $9,750 (55+ only...50-54 is $8,750)

Strategic Considerations for Those Nearing Retirement

1. Take Full Advantage of the Age 60-63 Window: If you're in this age range, take advantage of the increased 401(k) or 403(b) contributions limits to the extent possible. The enhanced contribution limits for those age 60-63 increases tax-advantaged savings potential.

2. Don't Overlook IRAs: Even with the smaller dollar amounts, IRAs offer valuable tax benefits and more investment flexibility than many workplace plans. The $8,600 annual limit still represents meaningful tax-advantaged growth potential over time.

3. Think of HSAs as Tax-Advantaged Retirement Accounts: If you can afford to pay medical expenses out-of-pocket or with other funds, consider using your HSA like a tax-advantaged retirement account. You can take tax-free withdrawals for medical expenses at any time. Also, after age 65, you can withdraw for non-medical expenses penalty-free (though you'll pay income tax, like a traditional IRA).

4. Coordinate Multiple Accounts: You can contribute to multiple account types simultaneously. For example, someone age 60 could potentially save $49,850 in 2026 by maxing out a 401(k) ($35,750), IRA ($8,600), and individual HSA ($5,400) if cash flow permits.

5. Start Planning Now: With these increases taking effect January 1, 2026, now is the time to review your cash flow and adjust your contribution rates for 2026. Spreading increased contributions across 12 months makes the higher limits more manageable.

The Bottom Line

The increased 2026 contribution limits provide meaningful increases for retirement savers age 50+, with the most significant advantage going to those between 60 and 63.

These enhanced limits arrive at a crucial time, as Americans are living longer and facing higher healthcare costs in retirement.

Whether you're five years from retirement or fifteen, taking advantage of these higher limits—especially the catch-up provisions—can make a substantial difference in your retirement security.

Every additional dollar you contribute today is a dollar that can grow tax-advantaged for your future.

Want To Discuss This Individually?

1 - For clients: Call or email me any time as always.

2 - For non-clients: Complete the form on the website to request a retirement planning consultation: www.rolekretirement.com

This is article is for informational purposes only and should not be considered as tax or legal advice. Advice is only provided after entering into an Advisory Agreement with the Advisor. See other disclosure here: Disclosures

Comments