The “Widow’s (or Widower's) Tax Trap” Many Couples Never Plan For

- Kyle Rolek, Retirement Planning Specialist

- May 18

- 4 min read

When most couples think about retirement planning, they picture things like investment performance, retirement income, healthcare costs, or estate documents.

Taxes are usually part of the conversation too.

But there’s one tax issue that often catches retirees completely off guard — and unfortunately, many families don’t discover it until after the loss of a spouse.

It’s sometimes called the “widow’s (or widower's) tax trap.”

And despite the name, it has nothing to do with making a mistake or doing something wrong.

In fact, this problem often affects couples who saved diligently, invested responsibly, and did many things exactly right over the course of their lives.

The issue is that after one spouse passes away, the surviving spouse can suddenly find themselves paying significantly higher taxes — even though household income may have declined.

At first glance, that doesn’t seem like it should happen. If there’s now one person instead of two, shouldn’t taxes go down?

In many cases, the opposite occurs.

One of the biggest reasons is the way tax brackets change after a spouse passes away.

Married couples filing jointly benefit from wider tax brackets and higher income thresholds.

But after the year of death, the surviving spouse typically transitions to filing as a single taxpayer. That change alone can create a major shift.

Imagine a retired couple with income coming from several sources: Social Security, required minimum distributions from IRAs, pension income, and investment earnings.

After one spouse dies, one Social Security check may disappear, but much of the remaining income often stays relatively intact.

The IRA distributions don’t suddenly vanish.

Pension income may continue at a reduced level.

Investment income may remain similar.

In some cases, the surviving spouse may still be receiving a large portion of the same household cash flow — but now under a much less favorable tax system.

As a result, income that once comfortably fit inside married filing joint tax brackets can suddenly spill into higher brackets for a single filer.

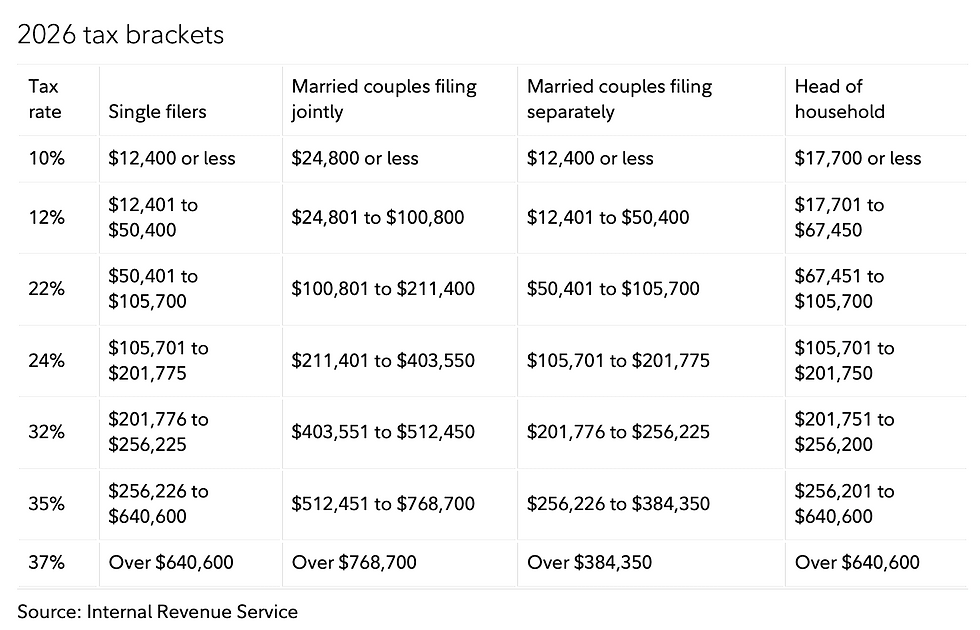

The image below shows single filer tax brackets on the left vs married couple filing jointly tax brackets from second to left.

As an example using $80k of taxable income:

As married filing jointly, the tax bracket is 12%

As single, the tax bracket is 22%

This can become especially painful for retirees with substantial pre-tax retirement accounts.

Ironically, the people most vulnerable to this issue are often disciplined savers.

Over decades, they contributed consistently to 401(k)s and IRAs, deferred taxes successfully, and allowed those accounts to grow.

But later in retirement, those larger account balances can create sizable required minimum distributions that continue regardless of whether one spouse has passed away.

We sometimes see situations where a surviving spouse has lower overall income than before, but a surprisingly high percentage of that income becomes taxable at elevated rates.

And taxes are only part of the problem.

Many retirees are surprised to learn that Medicare premiums can increase as well.

Medicare IRMAA surcharges are based on income thresholds, and those thresholds become significantly less forgiving for single filers.

A surviving spouse may suddenly find themselves paying higher Medicare Part B and Part D premiums simply because the rules are less favorable for individuals.

The image below shows thresholds for Medicare Part B premiums for individual filers on the left column and joint filers in the second to left column.

Joint filers need adjusted gross income to exceed $218k before they need to worry about paying higher premiums for Medicare.

Single filers need adjusted gross income to exceed $109k before they need to worry about paying higher premiums for Medicare.

In other words, the financial impact of losing a spouse can extend far beyond the emotional loss itself. The surviving spouse may experience:

Higher marginal tax rates

Higher Medicare premiums

Reduced Social Security income

Continued required distributions from retirement accounts

Less flexibility in managing taxable income

All of this can happen during one of the most emotionally difficult transitions of a person’s life.

The good news is that this issue can often be reduced with proactive planning.

One of the most effective opportunities frequently occurs in the years between retirement and required minimum distribution age.

During this window, some retirees may temporarily find themselves in relatively favorable tax brackets before Social Security, pensions, and RMDs fully stack together.

Those years can create opportunities for strategies such as Roth conversions, which may help reduce future taxable retirement income for the surviving spouse later on.

In some cases, couples may also benefit from carefully coordinating withdrawal strategies across different account types rather than simply pulling income from whichever account feels most convenient at the time.

The important point is not that every couple needs the same strategy. It’s that retirement planning is often far more interconnected than people realize.

Investment decisions affect taxes. Taxes affect Medicare premiums. Withdrawal decisions affect long-term flexibility. Social Security timing affects survivor income. Estate planning impacts the surviving spouse’s future financial picture.

These pieces don’t operate independently.

That’s one reason why retirement planning becomes increasingly important later in life — not less.

For many people, the accumulation years are relatively straightforward: save consistently, invest prudently, and avoid major mistakes.

But once retirement begins, the planning often becomes more nuanced. The order in which decisions are made can matter just as much as the decisions themselves.

No one enjoys discussing the possibility of losing a spouse.

But thoughtful planning today can potentially reduce financial stress for the surviving spouse years down the road.

And in many cases, addressing these issues proactively may create greater flexibility, lower lifetime taxes, and more peace of mind for both spouses while they’re still together.

Want To Discuss This Individually?

1 - For clients: Call or email me any time as always.

2 - For non-clients: Complete the form on the website to request a retirement planning consultation: www.rolekretirement.com

This article is for informational purposes only and should not be considered as tax or legal advice. Advice is only provided after entering into an Advisory Agreement with the Advisor.

Comments